Rent? or BUY…

The choice between renting or buying can be tough, but if you crunch the numbers, you may be surprised to find that a monthly mortgage payment is pretty close to what you’re paying in rent. It’s time to swap your rent payment for a mortgage that will pay YOU back in the form of equity.

The homeownership rate in America continues to rise, proving still that Americans prefer owning over renting. Why? Because of the investment value. Studies show that people who purchase a home before the age of 35 are better prepared for retirement at age 60. At retirement age, people rely more heavily on their wealth rather than their income to support their lifestyles.

Today’s young adults can prepare for retirement and build wealth through housing, the largest single source of wealth. People make the choice to own or rent based on what suits them at that given point, but before your extend your lease, maybe consider the long-term consequences of renting when homeownership is an option.

Study after study shows that no matter what generation Americans belong to, the vast majority believe that homeownership is an important part of their American Dream. Homeownership is a major milestone in ones life and provides the financial security to make a major investment and then watch it grow over time.

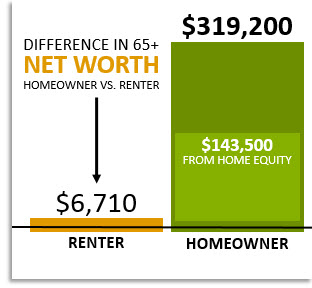

HOMEOWNERS NET WORTH 47.5% GREATER THAN RENTERS

The Joint Center for Housing Studies at Harvard University focused on homeowners and renters over the age of 65. Their study revealed a major difference in net worth between homeowners and renters, with a large portion coming from home equity! How does that work?

RISING RATES & NO SAVINGS

Rents are rising at a fast pace, and have been since the late 1980’s. Currently, the median rental rate sits at $1014 per month, up 147% since 1988. While making a rent payment, no tax benefit or earned equity is derived for the future, leaving less each month for a renter to save or invest. In fact, with each and every rent payment made, it’s the landlord who cashes in on those benefits.

EARNED EQUITY THAT GROWS

The major difference between a $1,000 rent & a $1,000 mortgage, is the accrual of equity. It is estimated that a homeowner making a $998 monthly mortgage payment (principle & interest) on a $200,000 home can accrue an estimated $3,021 in equity in year one, $3,436 in year two, growing year after year. In just 5 years, a homeowner will have accrued over $25,000 in earned equity & property appreciation!

Your monthly mortgage payment is a form of “forced savings” building your net worth with each and every payment.

Every market is different. Before you renew your lease, meet with a local REALTOR® and find out if you can put your rental costs to work for you. With a little research & help from a professional, you may find that owning a home is more affordable than renting!

DON'T WAIT! THE TIME IS NOW...

We’ve all been hearing the phrase ‘New Year, New You’ these last few months with intentions to make changes in self-improvement, finances, and to set goals, both large and small. This shift in mindset should apply to your goals of homeownership as well. If you’ve been renting for years, now is the time to meet with a professional REALTOR® to start the transition from renter to homeowner. A REALTOR® can help you determine your cost range for a home, map out your financial possibilities and parameters, find a home that fits your needs, and help you find the best mortgage options to make homeownership your reality this year. See below for 3 tips on preparing for homeownership.

HOW MUCH $$$ IS NEEDED… When asked why renters haven’t yet considered homeownership, saving for a down payment is cited as one of the biggest barriers. First things first, there are many loan programs available that require as little as 0-5% down, so don’t let the thoughts of a massive down payment deter you. This is where consulting with a REALTOR® becomes crucial. Once you identify how much is needed to buy a home, you can begin saving. You can jump start your savings by automating your checking account to auto-draft a small portion of each paycheck into your savings for the “homeownership fund.” It takes discipline & perseverance, but it can be done.

BUILD CREDIT HISTORY & KEEP IT CLEAN… When you go to apply for a mortgage, lenders will want to see that you are credit worthy, meaning you’ve been able to pay off past debts. This means staying on top of paying your student loans, credit cards & car loans on time. Some consumer debt will not disqualify you from getting a loan, but keeping debt low will help you maximize your home buying power. If you have not yet established credit history, CLICK HERE to learn 5 ways you can start building credit now.

PRACTICE LIVING ON A BUDGET… 95% of first time home buyers are willing to make sacrifices to buy their home faster. Some of those items include new clothes, traveling or forgoing that new car you’ve been eyeing. Downsizing your spending now will allow you to save more for your home purchase & pay down any consumer debt that will improve your credit score. Being a homeowner also means that repairs & upkeep are now your responsibility, so setting aside a monthly budget for the inevitable issues that crop up from time to time will help you prepare for the unexpected.